*

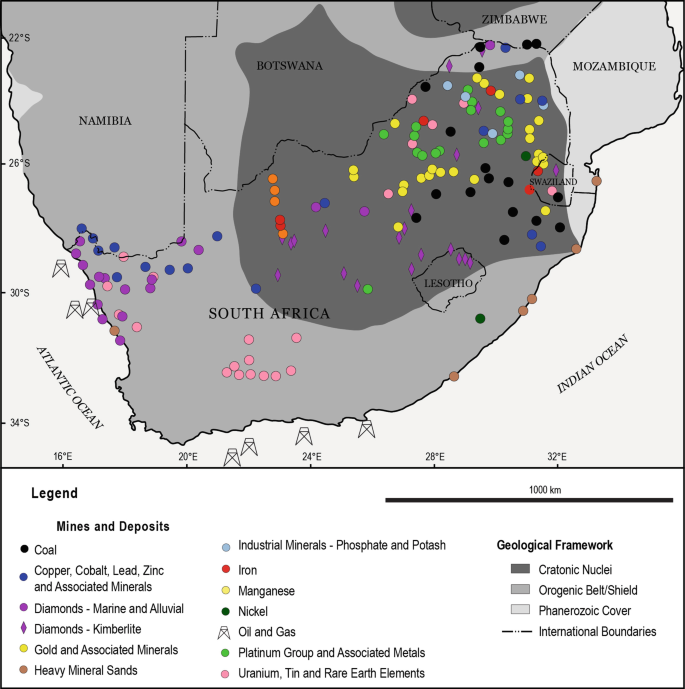

Betaal is die “wet van Transvaal”. Dis nie net in Transvaal waar belastings gehef en betaal word nie. Die hele land betaal dubbel en dwars belastings wat uitermatig hoog is. Eintlik teveel, veral as die minerale aan die een kant geweeg word met die handjievol belastingbetalers, wat meestal niks van die rykdomme deel nie. Alle lande ook buite ons grense, vra belasting en soms ook BTW (belasting op toegevoegde waarde). Ons geldwaarde is baie swak en dit wat mens koop, of wil koop is soms die helfte wat dit was 20 jaar gelede. Tog is daar vandag meer ryk swartes en die sogenaamde agtergeblewenes in 30 jaar wat multi-miljoenêrs geword. Die kaart wys nie alle minerale in Suid-Afrika aan nie.

*

Daar is wel meer armes in Suid-Afrika, maar ‘n groot meerderheid swartes wat die land binnestroom, ry op die kaartjie dat hulle Suid-Afrikaanse burgers is, maar dit nie is nie. Afrika is geseënd met minerale, maar so is Suid-Afrika ook. Net jammer die burgers van Suid-Afrika het nie toegang tot al die groot mineraal ontginnings, wat meestal landuit gevoer word.

Sedert 1880 het sioniste (mynmagnate as immigrante) hul ingewurm in die minerale bedryf in Suid-Afrika. Dis hulle wat destyds die president van ZAR probleme gegee het om burgerskap te kry en almal het hulle ryker gemaak uit ons minerale uit. Dit is ook grootliks hieroor wat die ABO plaasgevind het – om ‘n Boere volk te vernietig, die Boere republieke so in te palm vir al die minerale rykdom.

AFRIKA

https://www.theassay.com/articles/analysis/put-simply-the-world-needs-african-minerals/

Intussen krepeer die verskillende volke en beslis die Boere volk van die Boere republieke, wat inderwaarheid aan die Boere volk behoort. Hul reg tot vryheid is deur Brittanje en haar bondgenote gekaap in 1902, wat onregverdig is.

Die Boere volksgenote word gerieflik deur alle regerings sedert 1902 uit die ekonomie verban of om hoegenaamd hul posisie in die Boere republieke te herstel.

Invalsplanne op Boere republieke

Dit is onregverdig omdat al die ander volke, Khoi San, Griekwas en elke ander swart stam, hul kroongebiede en tuislande behou het, wat na 1994 omgeskakel is na Trust en KEV gebiede – dit is met behulp van nuwe ANC en Grondeise wetgewing gedoen. Die Boere het beslis nie die swartes se grondgebiede gesteel soos wat daar altyd beheer word nie. Hul het die BESETTE grondgebiede onderhandel, gekoop of geruil vir dienste wat gelewer is.

Trustgebiede – Tuislande – Reservate en Kroongebiede

*

‘n Berig van 2018.

MINERALE- EN PETROLEUM HULPBRONNE TANTIÈME

1 Oktober 2018 – Minerale- en Petroleum hulpbronne-tantièmeopgawe (MPR3) SARS het ‘n nuwe vorm in werking gestel vir minerale- en petroleum hulpbronne opgawe en betalingsadvies. Die vorm is beskikbaar vir aflaai vanaf 1 Oktober 2018 en die bestaande MPRR-belastingpligtiges sal verwag word om die nuwe MPRR opgawe en betalingsdata-vorm te voltooi:

o Die ou Minerale- en Petroleumhulpbronne-betalingsadvies (MPR2) en Minerale- en Petroleum hulpbronne-opgawe (MPR3) is in een Minerale- en Petroleumhulpbronne-opgawe (MPR3) geïnkorporeer. Om te verklaar, moet die nuwe MPR3-opgawe voltooi word.

o Die MPR3-opgawe is opgedateer met die mineraalsoort, eenheid van meting en volume oorgedra (hoeveelheid), van mineraal verkoop, wat voorheen nie in die MPR3 ingesluit was nie.

o Die MPR3-vorm is gestandaardiseer om vir al die eienskappe voorsiening te maak, naamlik indienings-, betalings- en opgaweverpligtinge hieronder:

Betalings kan gemaak word deur die eFiling “Additional Payment” funksie (ook na verwys as “Ad Hoc” betaling) of “SARS Other” vir EFO-betaling, pas die 19-syferreël toe (TAXREFNUMBX00000155) en elke betaling moet vergesel wees deur die voltooide Minerale- en Petroleum hulpbronne tantièmeopgawe (MPR3).

o Betalings moet verkieslik deur eFiling gemaak word, na die SARS-rekening, en elke betaling moet deur ‘n voltooide MPR3-opgawe vergesel wees.

o Betalings kan ook deur die bankkanaal gemaak word (nie die verkiesde kanaal nie), deur EFO en hierdie metode vereis die toepassing van die 19-syferreël (TAXREFNUMBX00000155).

Top wenk: Belastingpligtiges word aangemoedig om so spoedig as moontlik na eFiling as

betalingskanaal oor te skakel. Die bankkanale sal op 31 Januarie 2019 afgeskaf word vir

MPRR-betalings, wat beteken dat alle MPRR-betalings slegs deur die eFiling-kanaal

gemaak sal kan word.

Jy kan hieronder toegang tot die opgedateerde MPRR eksterne gids en MPR3-vorm verkry:

Mineral and Petroleum Resources Royalties External Guide

MPR3 Mineral and Petroleum Resources Royalty Return External Form

Wat is dit?

In die verlede was minerale- en petroleumhulpbronne in privaat besit en dus die betaling vir ontginning van hierdie hulpbronne slegs onder bepaalde omstandighede aan die staat betaalbaar, bv. waar ontginning op staatsgrond plaasgevind het.

Om Suid-Afrika in lyn te bring met heersende internasionale norms, het die Departement van Minerale en Energie die Wet op Ontwikkeling van Minerale- en Petroleumhulpbronne, 2002, (MPRDA) bekendgemaak, ingevolge waarvan hierdie hulpbronne as die gemene nalatenskap van al die mense van Suid-Afrika erken word, met die staat as bewaarder daarvan tot voordeel van alle Suid-Afrikaners.

Die minister van finansies moet, ingevolge artikel 3(4) van die MPRDA, die staatsheffing

bepaal en ophef by wyse van ‘n parlementswet. Die minister het dit gedoen deur die

bekendstelling van die Wet op Minerale- en Petroleumhulpbronne-tantième, 2008, asook die Wet op Minerale- en Petroleumhulpbronne-tantième (Administrasie), 2008, wat beide deur SARS geadministreer word.

Die tantième tree in werking met die oordrag van mineraalregte, uit die Republiek afkomstig.

Soos in die geval van alle ander belastings, regte, heffings, fooie of geld deur SARS

ingevorder, word die ingevorderde tantième aan die Nasionale Inkomstefonds betaal

Vir wie is dit?

Die volgende persone moet vir die betaling van hierdie tantième by SARS registreer:

Enige persoon wat ‘n prospekteerreg, retensiepermit, verkenningsreg, mynreg,

mynpermit of produksiereg of ‘n huurkontrak of onderverhuringskontrak ten opsigte

van sodanige reg het; of

Enige persoon wat ‘n mineraalhulpbron, wat binne die Republiek ontgin is, wen of

herwin.

Watter stappe moet ek volg?

‘n Aansoekvorm (MPR1) moet voltooi word. Dit is hieronder beskikbaar en kan ook by enige

SARS-tak verkry word. Sodra voltooi, moet dit geskandeer en per e-pos gestuur word aan

mineralroyalty@sars.gov.za. Die voltooide MPR3-vorm moet ook per e-pos gestuur word

aan mineralroyalty@sars.gov.za.

Wat is die koers vir die tantième?

Die koers vir die tantième word bepaal volgens ‘n formule soos uiteengesit in subafdelings

(1) en (2) van artikel 4 van die Wet op Minerale- en Petroleumhulpbronne-tantième, 2008 en tref onderskeid tussen die veredelde en onveredelde kondisies van die mineraalbronne en is tans as volg:

vir veredelde mineraalbronne: die minimum van 0.05% tot ‘n maksimum van 5%

vir onveredelde mineraalbronne: die minimum van 0.5% tot ‘n maksimum van 7%.

Wanneer en hoe moet die tantième betaal word?

Betalings kan deur die eFiling-kanaal gemaak word deur die gebruik van die “Additional

Payment” opsie. Neem kennis dat bankkanale vir MPRR-betalings op 31 Januarie 2019

afgeskaf sal word, wat beteken dat alle MPRR-betalings slegs deur die eFiling-kanaal

gemaak sal kan word. Maak asseblief seker dat die eFiling-kanaal vir elke MPRR belastingpligtige opgestel is en begin om alle betalings deur hierdie kanaal te maak om seker te maak dat daar geen moeilikhede voorkom wanneer bankkanale afgeskaf word nie.

Neem kennis dat elke betaling deur ‘n voltooide MPR3 (nuwe) vorm vergesel moet wees,

soos vereis deur wetgewing, vir die twee voorlopige betalings, die derde oorskotbetaling en die finale opgawe (indien verdere betaling nodig is).

http://www.sars.gov.za/TaxTypes/MPRR/Pages/default.aspx

***

How is SARS procurement governed?

SARS’ Procurement and Supply Chain Management processes are subject to the provisions of;

-

the Public Finance Management Act No.1 of 1999 (PFMA)

-

the Treasury Regulations for departments, trading entities ,constitutional institutions and public entities, 2005 issued in terms of the PFMA

-

the Preferential Procurement Policy Framework Act No. 5 of 2000 (PPPFA)

-

the Preferential Procurement Regulations, 2011 issued in terms of the PPPFA

-

the Supply Chain Management practice notes, instruction notes and circulars issued by National Treasury from time to time

-

SARS’ internal delegations of authority

***

MINERAL AND PETROLEUM RESOURCES ROYALTY

What’s New?

- 01 October 2018 – Mineral and Petroleum Resource Royalties Return (MPR3)

SARS rolled out a new form for Mineral and Petroleum Resources Return and Payment advice. The form is available to download from 01 October 2018 and the existing MPRR taxpayers will be expected to complete the new MPRR return and payment data form:- The old Mineral and Petroleum Resources Payment advice (MPR2) and Mineral and Petroleum Resources Return (MPR3) have been incorporated into one Mineral and Petroleum Resources Return (MPR3), to declare you must complete the new Return (MPR3).

- The return MPR3 has been updated with the type of mineral type, unit of measure and volume transferred (quantity) of mineral sold which was previously not included in the MPR3.

- The MPR3 form has been standardised to cater for all the attributes namely filing, payment and return obligations below:

-

- Payments can be made via eFiling Additional Payment function (also referred to as “Ad Hoc” payment) or ‘SARS Other’ when it comes to EFT, apply the 19-digit rule (TAXREFNUMBX00000155) and each payment must be accompanied by the completed Mineral and Petroleum Resources Royalty return (MPR3).

- Payments must preferably be made via eFiling into the SARS account and each payment must be accompanied by a completed return (MPR3).

- Payments can also be made via the bank channel (not preferred channel), by using EFT and this method requires application of the 19 digit rule (TAXREFNUMBX00000155).

Top tip: Taxpayers should be urged to move to eFiling as a payment channel as soon as possible. The bank channels (EFT and over the counter payments) will be discontinued for MPRR during the first Quarter of 2019, which implies that all MPRR payments will only be payable by using the eFiling channel in future.

You can access the updated MPRR external guide and MPR3 form below:

- Mineral and Petroleum Resources Royalties External Guide

- MPR3 Mineral and Petroleum Resources Royalty Return External Form

What is it?

In the past, mineral and petroleum resources were privately owned, meaning that payment for the extraction of these resources was payable to the State only under certain circumstances, e.g. where mining had been conducted on State-owned land.To bring South Africa in line with prevailing international norms, the Department of Minerals and Energy promulgated the Mineral and Petroleum Resources Development Act, 2002 (MPRDA) in terms of which these resources are recognised as the common heritage of all the people of South Africa with the State as custodian thereof for the benefit of all South Africans.The Minister of Finance must, in terms of section 3(4) of the MPRDA determine and levy the State royalty by means of an Act of Parliament. This the Minister did by promulgating the Mineral and Petroleum Resources Royalty Act, 2008 as well as the Mineral and Petroleum Resources Royalty (Administration) Act, 2008, both of which are administered by SARS.The royalty is triggered on the transfer of a mineral royalty extracted from within the Republic. As is the case for all other taxes, duties, levies, fees or money collected by SARS, the royalty collected is paid to the National Revenue Fund.Who is it for?

The following persons must register for the payment of the royalty to SARS:- Any person who holds a prospecting right, retention permit, exploration right, mining right, mining permit or production right or a lease or sublease in respect of such a right; or

- Any person who wins or recovers a mineral resource extracted from within the Republic.

What steps must I take?

An application form MPR1 must be completed. It is available below and can also be obtained at any SARS branch. Once completed, it must be scanned and emailed to mineralroyalty@sars.gov.za. The completed MPR3 form must also emailed to mineralroyalty@sars.gov.za.What is the rate for the royalty?

The rate for the royalty is determined according to a formula contemplated in subsections (1) and (2) of section 4 of the Mineral and Petroleum Resources Royalties Act, 2008 and differentiates between the refined and unrefined conditions of the mineral resource, and are currently as follows –- for refined mineral resources: the minimum of 0.5% to a maximum of 5%

- for unrefined mineral resources: the minimum of 0.5% to a maximum of 7%.

When and how should the royalty be paid?

Payments can be made via the eFiling channel using the Additional payment option. Note that bank channels will be discontinued for MPRR payments on 31 January 2019, which implies that all MPRR payments will only be payable by using the eFiling channel. Please ensure that the eFiling channel is set up for each MPRR taxpayer and start making all payment via this channel to ensure no issues are experienced when banking channels are discontinued.Note that each payment must be accompanied by a completed MPR3 (new) form as required by legislation for the two provisional payments, the third excess payment and the final return (if a further payment is necessary).

Contact Admin

Admin kan gekontak word by

volksvryheid9@gmail.co -

[…] Minerale regte, belasting en regering […]

LikeLike

[…] Minerale regte, belasting en regering […]

LikeLike

[…] Minerale regte, belasting en regering […]

LikeLike

[…] Minerale regte, belasting en regering […]

LikeLike

[…] Minerale regte, belasting en regeringHoe lyk die land nie verwaarloos met doelgerigte misdaad en agteruitgang nie.* […]

LikeLike